Gifting and the Custom Contract of Life insurance

Gifting and the Custom Contract of Life Insurance

By: Peter R. Moison, J.D., TEP, President

Why take advantage of the one-time ability to make a five million dollar gift this year without paying gift tax? The benefit of making such a gift is the future appreciation of the gifted property will not be subject to estate tax when the donor dies. This is potentially a huge benefit if the client lives a long time. Therefore, any plan to make such a gift should take into consideration how to get the tax benefit, regardless of when the client dies, and how to maximize the functional utility of the gifted property in the hands of the beneficiaries.

The potential problems:

- If the client dies before the gifted property increases in value little or nothing has been gained by making the gift. The reason is the “gross up” provision in the estate tax rules that require the taxable estate of the donor to be increased by any and all taxable gifts made. Thus the $5M gift will be subject to estate tax when the donor dies, no matter when death occurs. So the key is to find a way to “realize” the appreciation even if the client dies too soon.

- Let’s assume the best and the donor lives a long time and the gifted property appreciates substantially in value. This issue now becomes how can the beneficiaries use that property should a need arise? If the property is sold then capital gains tax will be imposed on any gain. If the property is borrowed against then the interest will generally be paid to an unrelated creditor. Both of these problems can be solved with the proper planning.

A customized contract approach to life insurance solves both of the above issues on an extremely cost effective basis.

Problem of death occurring before the gifted property increases in value

This issue can be explored with the client in advance of the gift. If the client is concerned about the same then a customized life insurance contract (“CCL”) can be designed so the death benefit creates a substantial gain to the beneficiaries if death occurs too soon. At a minimum the benefits are as follows:

- The CCL is self completing in the event of an early death

- The gain from the CCL is both income and capital gains tax free

- The CCL gain is not added back to the donor’s estate for estate tax purposes

- CCL insurance proceeds are free from any creditor claims against the donor or his/her estate.

Efficient use of the gifted property

There are two great non tax benefits of making gifts. First the donor gets to see the beneficiaries enjoy the benefits of the gifted property if the gift is set up to allow the same. The second is the gifted property can serve as a valuable safety net should the same be needed if financial circumstances change in the future. Traditionally, however, there are some tax and other issues that should be considered.

- Can the gifted property help to further reduce the estate tax on the property that remains in the donor’s estate?

- If there is a need to use the property what are the income tax consequences on any gain?

- Can the property be borrowed against? If so, who gets the benefit of the interest paid on the loan? What will the terms/restrictions of the loan be? And can a loan even be arranged?

A properly thought out and designed CCL life insurance solution can prevent any issues set out above from preventing either the enjoyment of the gifted property or the safety net value of the gift. In addition a CCL solution has the potential to help with future estate tax planning for the donor in order to further reduce the taxable estate. If the property needs to be used a properly designed and administered CCL can provide the following benefits:

- No tax imposed on any gain

- If there is a need to borrow against the property interest paid on the loan will enhance the CCL solution

- No loan rejection; no lien imposed on the loan; and no benefit to a third party creditor

- The CCL can be designed to help further reduce the estate tax and to coordinate with other estate planning techniques

Cost Efficiency

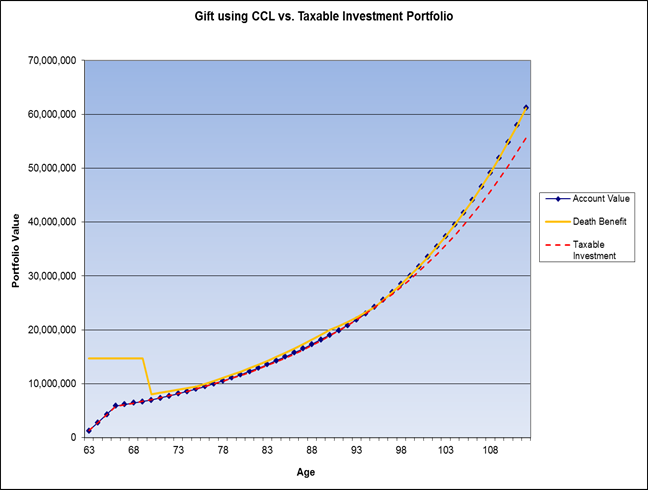

While the above all sounds good a legitimate question is: are the total costs of the CCL more than tax cost to use a taxable investment portfolio? The answer is ‘no’. A CCL solution should actually save money over time as opposed to costing money. Take a look at the following chart:

The chart shows what could happen if the funds are invested in a typical long term investment portfolio. It is assumed the investment portfolio is the same for both the CCL and the taxable investment. The rate of return shown is 6% per annum and the taxable portfolio reflects the typical annual tax consequence. The CCL is net of all costs. While the numbers look very close the taxable portfolio will have a significant amount of capital gain that will eventually be taxed. The capital gains tax is not reflected in the chart. In contrast as long as the CCL is not surrendered the entire growth will eventually be delivered both income and estate tax free with the result you can expect no capital gains tax offset with the CCL. The CCL also provides a significant safety net that allows access to the reserve (cash value) that is income tax free.

Therefore, a further answer to the question above about cost: is the tax cost of the taxable portfolio greater than the cost of the CCL. All things being equal the CCL will deliver more overall benefit and utility to the family than a similar or identical taxable portfolio.

The content, ideas, phrases, and expressions “Advised Life”, “custom contract life insurance”, “New Standard”, “CCL” no matter what form they are in or font used are the exclusive property of Castle Re Insurance Company, Ltd. PCC and the author. No part of this article may be reproduced in whole or in part without the expressed written consent of Castle Re Insurance Company, Ltd. PCC or the author.

Gifting and the Custom Contract of Life insurance

2012 05 28 Gifting and the Custom Contract of Life Insurance

By: Peter R. Moison, J.D., TEP, President

Why take advantage of the one-time ability to make a five million dollar gift this year without paying gift tax? The benefit of making such a gift is the future appreciation of the gifted property will not be subject to estate tax when the donor dies. This is potentially a huge benefit if the client lives a long time. Therefore, any plan to make such a gift should take into consideration how to get the tax benefit, regardless of when the client dies, and how to maximize the functional utility of the gifted property in the hands of the beneficiaries.

The potential problems:

- If the client dies before the gifted property increases in value little or nothing has been gained by making the gift. The reason is the “gross up” provision in the estate tax rules that require the taxable estate of the donor to be increased by any and all taxable gifts made. Thus the $5M gift will be subject to estate tax when the donor dies, no matter when death occurs. So the key is to find a way to “realize” the appreciation even if the client dies too soon.

- Let’s assume the best and the donor lives a long time and the gifted property appreciates substantially in value. This issue now becomes how can the beneficiaries use that property should a need arise? If the property is sold then capital gains tax will be imposed on any gain. If the property is borrowed against then the interest will generally be paid to an unrelated creditor. Both of these problems can be solved with the proper planning.

A customized contract approach to life insurance solves both of the above issues on an extremely cost effective basis.

Problem of death occurring before the gifted property increases in value

This issue can be explored with the client in advance of the gift. If the client is concerned about the same then a customized life insurance contract (“CCL”) can be designed so the death benefit creates a substantial gain to the beneficiaries if death occurs too soon. At a minimum the benefits are as follows:

- The CCL is self completing in the event of an early death

- The gain from the CCL is both income and capital gains tax free

- The CCL gain is not added back to the donor’s estate for estate tax purposes

- CCL insurance proceeds are free from any creditor claims against the donor or his/her estate.

Efficient use of the gifted property

There are two great non tax benefits of making gifts. First the donor gets to see the beneficiaries enjoy the benefits of the gifted property if the gift is set up to allow the same. The second is the gifted property can serve as a valuable safety net should the same be needed if financial circumstances change in the future. Traditionally, however, there are some tax and other issues that should be considered.

- Can the gifted property help to further reduce the estate tax on the property that remains in the donor’s estate?

- If there is a need to use the property what are the income tax consequences on any gain?

- Can the property be borrowed against? If so, who gets the benefit of the interest paid on the loan? What will the terms/restrictions of the loan be? And can a loan even be arranged?

A properly thought out and designed CCL life insurance solution can prevent any issues set out above from preventing either the enjoyment of the gifted property or the safety net value of the gift. In addition a CCL solution has the potential to help with future estate tax planning for the donor in order to further reduce the taxable estate. If the property needs to be used a properly designed and administered CCL can provide the following benefits:

- No tax imposed on any gain

- If there is a need to borrow against the property interest paid on the loan will enhance the CCL solution

- No loan rejection; no lien imposed on the loan; and no benefit to a third party creditor

- The CCL can be designed to help further reduce the estate tax and to coordinate with other estate planning techniques

Cost Efficiency

While the above all sounds good a legitimate question is: are the total costs of the CCL more than tax cost to use a taxable investment portfolio? The answer is ‘no’. A CCL solution should actually save money over time as opposed to costing money. Take a look at the following chart:

The chart shows what could happen if the funds are invested in a typical long term investment portfolio. It is assumed the investment portfolio is the same for both the CCL and the taxable investment. The rate of return shown is 6% per annum and the taxable portfolio reflects the typical annual tax consequence. The CCL is net of all costs. While the numbers look very close the taxable portfolio will have a significant amount of capital gain that will eventually be taxed. The capital gains tax is not reflected in the chart. In contrast as long as the CCL is not surrendered the entire growth will eventually be delivered both income and estate tax free with the result you can expect no capital gains tax offset with the CCL. The CCL also provides a significant safety net that allows access to the reserve (cash value) that is income tax free.

Therefore, a further answer to the question above about cost: is the tax cost of the taxable portfolio greater than the cost of the CCL. All things being equal the CCL will deliver more overall benefit and utility to the family than a similar or identical taxable portfolio.

The content, ideas, phrases, and expressions “Advised Life”, “custom contract life insurance”, “New Standard”, “CCL” no matter what form they are in or font used are the exclusive property of Castle Re Insurance Company, Ltd. PCC and the author. No part of this article may be reproduced in whole or in part without the expressed written consent of Castle Re Insurance Company, Ltd. PCC or the author.