Death Benefit Design

By:

Peter R. Moison, J.D. TEP, President

When it comes to the design of death benefit sometimes the obvious is the most elusive. Let’s think about the obvious in terms of insurance—any insurance. If an insurance company decides to insure a risk, it only does so if it has determined the chance of the risk turning into a claim any time soon is very small. This basic tenant is especially true when it comes to life insurance. Unlike other forms of insurance car or home owners for example life insurance is finite. Finite means the risk will result in a claim, the only question is when the claim will arise. We are all going to die whereas we all may not be involved in a car accident or have a need to make a claim on our home owners insurance. Thus the life insurance risk will eventually become a claim, provided the life insurance contract is in force when death occurs. To get really basic no life insurance company is going to agree to insure someone’s life unless they are convinced that person is going to live a really long time. The obvious, therefore, is the death benefit should be designed to be at its maximum when it is needed the most—when you are most likely to die which is late in life.

If you are a high net worth client who believes life insurance should be part of your long term estate and financial planning then your life insurance contract should not be designed backwards. Traditional life insurance policies do exactly that. The death benefit is designed to be the maximum up front and remain level for as long as the policy stays on the books. Such a design not only adversely impacts the long term viability of the life insurance policy it also means all the other benefits that are helpful to the high net worth client and his/her family are not only minimized but are also probably temporary. Proper design and timing of the maximum death benefit also helps assure all the other benefits will be maximized and a permanent part of the client’s overall estate and financial planning.

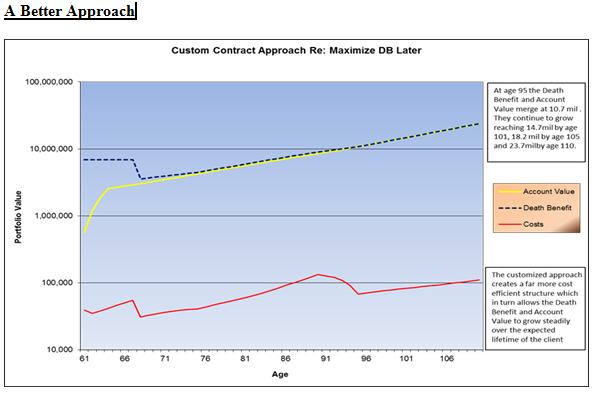

Let’s take a look at two different approaches: the traditional approach that is sold to most insurable clients; and a customized approach that is designed to help maximize the death benefit when the insurable high net worth client is expected to die. All the facts and variables used are identical—same premium, age, rating, assumed rate of return (6% per annum), and cost factors. The only difference is how the death benefit is designed. A custom designed approach means the final contract of life insurance will be completed in a manner that best fits the high net worth client’s long term estate and financial planning objectives. What is remarkable is how different the outcome is even though the cost and rate of return factors are the same. The custom approach that promotes cost efficiency is the key to the better outcome for the client and the client’s family. No company understands this better than CastleRE. That is why the tax attorneys behind CastleRE put CastleRE together. Life insurance has far too much potential to help the high net worth client. That potential should not be wasted.

.png)

A true custom designed approach means the final contract of life insurance will be completed in a manner that best fits the high net worth client’s long term estate and financial planning objectives. Only CastleRE takes the approach that written contract and the numbers are finalized in a custom drafted contract only after the client and the client’s advisory team is satisfied that the client’s objectives have been properly met. It is the New Standard for life insurance.

The content, ideas, phrases, and expressions “Advised Life”, “custom contract life insurance”, “New Standard”, no matter what form they are in or font used are the exclusive property of Castle Re Insurance Company, Ltd. PCC and the author. No part of this article may be reproduced in whole or in part without the expressed written consent of Castle Re Insurance Company, Ltd. PCC or the author.

Death Benefit Design

2012 05 17 By:

Peter R. Moison, J.D. TEP, President

When it comes to the design of death benefit sometimes the obvious is the most elusive. Let’s think about the obvious in terms of insurance—any insurance. If an insurance company decides to insure a risk, it only does so if it has determined the chance of the risk turning into a claim any time soon is very small. This basic tenant is especially true when it comes to life insurance. Unlike other forms of insurance car or home owners for example life insurance is finite. Finite means the risk will result in a claim, the only question is when the claim will arise. We are all going to die whereas we all may not be involved in a car accident or have a need to make a claim on our home owners insurance. Thus the life insurance risk will eventually become a claim, provided the life insurance contract is in force when death occurs. To get really basic no life insurance company is going to agree to insure someone’s life unless they are convinced that person is going to live a really long time. The obvious, therefore, is the death benefit should be designed to be at its maximum when it is needed the most—when you are most likely to die which is late in life.

If you are a high net worth client who believes life insurance should be part of your long term estate and financial planning then your life insurance contract should not be designed backwards. Traditional life insurance policies do exactly that. The death benefit is designed to be the maximum up front and remain level for as long as the policy stays on the books. Such a design not only adversely impacts the long term viability of the life insurance policy it also means all the other benefits that are helpful to the high net worth client and his/her family are not only minimized but are also probably temporary. Proper design and timing of the maximum death benefit also helps assure all the other benefits will be maximized and a permanent part of the client’s overall estate and financial planning.

Let’s take a look at two different approaches: the traditional approach that is sold to most insurable clients; and a customized approach that is designed to help maximize the death benefit when the insurable high net worth client is expected to die. All the facts and variables used are identical—same premium, age, rating, assumed rate of return (6% per annum), and cost factors. The only difference is how the death benefit is designed. A custom designed approach means the final contract of life insurance will be completed in a manner that best fits the high net worth client’s long term estate and financial planning objectives. What is remarkable is how different the outcome is even though the cost and rate of return factors are the same. The custom approach that promotes cost efficiency is the key to the better outcome for the client and the client’s family. No company understands this better than CastleRE. That is why the tax attorneys behind CastleRE put CastleRE together. Life insurance has far too much potential to help the high net worth client. That potential should not be wasted.

A true custom designed approach means the final contract of life insurance will be completed in a manner that best fits the high net worth client’s long term estate and financial planning objectives. Only CastleRE takes the approach that written contract and the numbers are finalized in a custom drafted contract only after the client and the client’s advisory team is satisfied that the client’s objectives have been properly met. It is the New Standard for life insurance.

The content, ideas, phrases, and expressions “Advised Life”, “custom contract life insurance”, “New Standard”, no matter what form they are in or font used are the exclusive property of Castle Re Insurance Company, Ltd. PCC and the author. No part of this article may be reproduced in whole or in part without the expressed written consent of Castle Re Insurance Company, Ltd. PCC or the author.